With effect from January 1, 2024, the amendment to the Act no. 563/2009 Coll. as amended (“Tax Code”) came into force and defines the so-called “second chance institute” which is applied by the tax and customs authorities.

The second chance institute means that the taxpayer will not be sanctioned for the first violation one of the offenses covered by this regulation. The tax administrator will ask the taxpayer for the first violation to comply with the obligations without imposing a penalty. Any further violation however will result in a penalty.

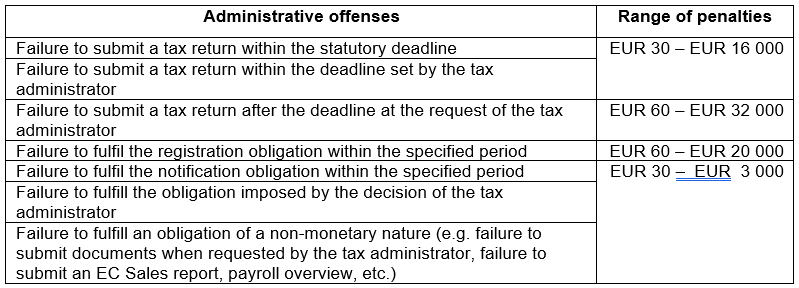

The second chance institute applies only to the administrative offenses for which the penalty is imposed within the specified range and which occurred after December 31, 2023.